For years, cryptocurrency was treated as a separate financial universe — a place of speculation, volatility, and digital coins with no clear connection to anything you could touch. That is changing fast. In 2026, one of the most powerful trends quietly reshaping global finance is real-world asset tokenization, often shortened to RWA.

Tokenization takes something with real value in the offline world — a U.S. Treasury bond, a slice of a building, a barrel of oil, a private credit loan — and represents that value as a token on a blockchain. Suddenly, traditionally slow, paperwork-heavy assets can move at internet speed, settle in seconds, and reach investors who were previously locked out by minimums or geography.

This guide breaks down what RWA tokenization actually is, why major institutions are pouring resources into it this year, the categories of assets being tokenized, the benefits and risks, and what it could mean for ordinary investors over the next few years.

What Does “Tokenization” Actually Mean?

At its simplest, tokenization is the process of creating a digital representation of an asset on a blockchain. The token isn’t just a picture or a number — it carries legal claims, ownership records, and programmable rules.

Think of it like converting a paper stock certificate into a digital share that lives on a public ledger. The blockchain becomes the system of record. Smart contracts handle distributions, dividends, transfers, and compliance checks automatically.

Three things make a tokenized asset different from a traditional one:

- Settlement is near-instant. Bond trades that take two business days in traditional markets can clear in seconds on-chain.

- Ownership is divisible. A million-dollar property can be split into thousands of fractional tokens, opening access to small investors.

- It runs around the clock. Traditional markets close. Blockchains do not.

Why 2026 Is the Breakout Year for RWAs

Tokenization isn’t new — banks and fintech firms have been experimenting with it since 2017 — but several forces are converging right now to push it from pilot projects into real production.

1. Regulatory clarity has finally arrived. In the United States, comprehensive stablecoin legislation passed in 2025 created the first clear federal framework for digital dollar tokens. The European Union’s MiCA regulation is now fully in force. Singapore, Hong Kong, and the United Arab Emirates have built dedicated licensing regimes for tokenized assets. For institutions that need legal certainty before deploying capital, the green lights are turning on.

2. Institutional infrastructure is mature. Qualified custodians, audit firms, and compliance tooling now exist at the level required by pension funds and asset managers. The “duct tape and hope” phase of crypto infrastructure is over for serious players.

3. The yield environment makes it attractive. Tokenized money market funds and on-chain Treasury products let investors earn traditional fixed-income yields while keeping the flexibility of a crypto wallet. That combination didn’t exist five years ago.

4. Major banks are issuing on public chains. When global banks start putting deposit tokens on public blockchains and partnering with crypto-native firms for settlement, the line between “TradFi” and “DeFi” begins to blur in a permanent way.

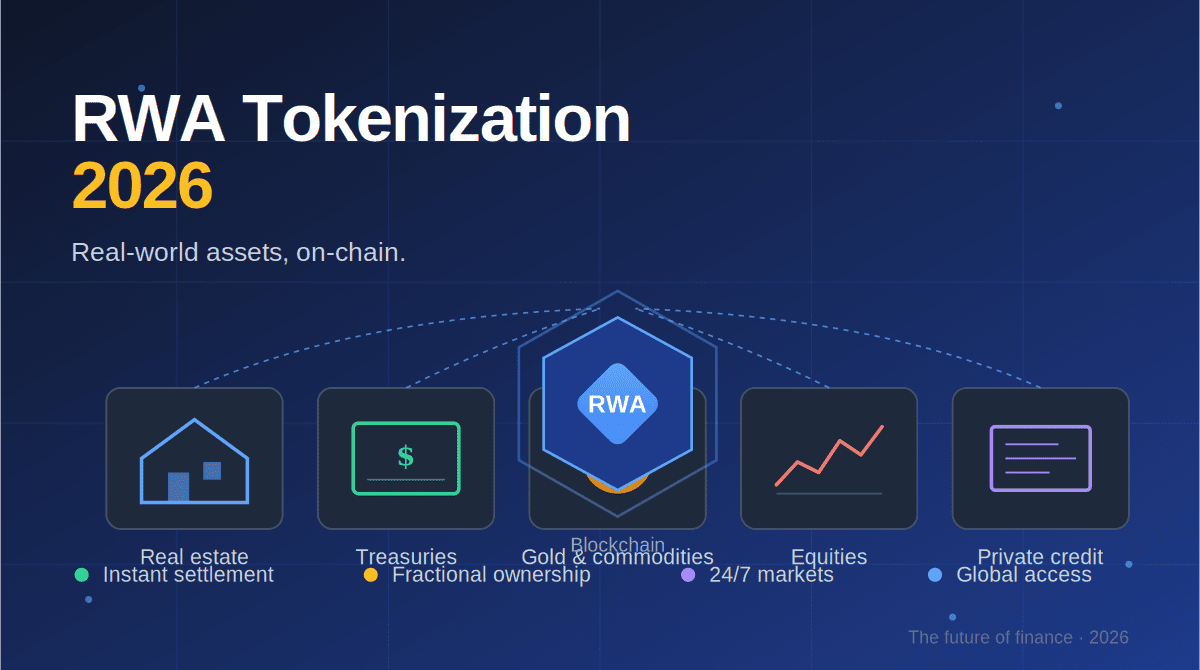

The Main Categories of Tokenized Real-World Assets

Not every asset is being tokenized at the same speed. Some categories are racing ahead while others remain experimental. Here is how the landscape looks in 2026.

Tokenized Treasuries and Money Market Funds

This is the largest and most mature category. Investors deposit cash, receive a token, and that token represents a claim on a basket of short-duration government debt. Yields flow back to token holders automatically. For corporate treasuries and crypto-native funds that already hold stablecoins, swapping into a yield-bearing tokenized treasury is now a routine cash management decision.

Stablecoins (the Foundation Layer)

Stablecoins are technically a form of tokenized money — usually backed one-for-one by dollars or short-term assets. They are now the most-used product in all of crypto, with monthly transaction volumes that rival major card networks. They serve as the rails for almost everything else in the RWA economy.

Tokenized Private Credit

Private credit — loans made outside the public bond market — has historically been illiquid and reserved for large institutions. On-chain, these loans can be packaged, fractionalized, and traded between qualified investors with far less friction. Several platforms now specialize in originating loans directly on-chain rather than wrapping off-chain agreements after the fact.

Tokenized Real Estate

This category captures the public imagination but is harder to scale. Tokens can represent fractional ownership in a single building, a portfolio of rental properties, or a real estate investment trust. The challenge is legal: property law is local, and getting tokens to legally confer the rights you would expect from a deed requires careful structuring jurisdiction by jurisdiction.

Tokenized Commodities

Gold-backed tokens were among the earliest RWAs and remain popular. More recently, oil, agricultural products, and even carbon credits have been tokenized, though liquidity outside of gold is still limited.

Tokenized Equities and Funds

Some jurisdictions now allow tokenized versions of public stocks or fund shares. These give investors exposure to traditional equity returns through a wallet rather than a brokerage account, with the same kind of 24/7 settlement other RWAs enjoy.

The Benefits: Why Anyone Cares About This

Tokenization is not interesting because of the technology — it’s interesting because of what the technology enables.

Lower minimums. A young investor in a developing country can buy ten dollars of a tokenized U.S. Treasury fund. Traditionally that product would have required a brokerage account, paperwork, and often a four- or five-figure minimum.

Faster settlement. Reducing the time between a trade and final settlement from two days to two seconds frees up enormous amounts of working capital across the financial system.

Programmable compliance. Smart contracts can enforce rules — like only allowing certain investors to hold a token, or automatically calculating tax events — without manual back-office work.

Composability. Once an asset is on-chain, it can plug into other on-chain systems. A tokenized treasury can be used as collateral for a loan, supplied to a liquidity pool, or bundled into a structured product, all without leaving the blockchain.

Transparency. Anyone can verify on a public blockchain that the supply of a token matches what is reported. That kind of real-time auditability is a step change from quarterly filings.

The Risks You Should Understand

Tokenization solves real problems but also introduces new ones. A balanced view requires looking at both sides.

Smart contract risk. The code that governs a token can have bugs. Major hacks have drained hundreds of millions of dollars from protocols over the years. Audited code reduces this risk but does not eliminate it.

Custody and counterparty risk. A token is only as good as the entity holding the underlying asset. If a tokenized treasury issuer goes bankrupt, the legal claim on the underlying bonds matters enormously. Different products have different bankruptcy protections.

Liquidity risk. Many RWA tokens trade on relatively thin markets. Selling quickly during stress can be hard, and the on-chain price can drift from the value of the underlying asset.

Regulatory risk. Despite progress, regulation is still patchy across jurisdictions. A token that is legal to hold in one country may not be in another. Investors should check their local rules before participating.

Oracle and data risk. Tokens that track off-chain assets rely on data feeds (called oracles) to bring real-world prices on-chain. A bad data feed can cause mispricing or even liquidations in connected lending markets.

What This Means for Everyday Investors

If you are not a hedge fund, why should you care about RWAs?

A few practical takeaways:

- Cash management is changing. If you already use stablecoins, a tokenized money market fund may offer a safer and more productive alternative for idle balances. Always read the disclosures.

- Access is expanding. Asset classes that were once gated — private credit, certain real estate funds, slices of fine art — are slowly becoming available at smaller sizes through tokenized formats. The rules vary by country.

- The line between brokerage and wallet is dissolving. Several mainstream fintech apps now let users hold tokenized versions of traditional assets without ever opening a separate crypto exchange account.

- Regulation is your friend, not your enemy. Products that comply with stablecoin or securities laws in your jurisdiction tend to be safer than those that operate in legal grey zones, even if their yields are lower.

How to Approach RWA Tokens Sensibly

If you decide to explore tokenized real-world assets, a few principles can save you a lot of trouble.

Start with the boring end of the spectrum. Tokenized cash and tokenized treasuries from regulated issuers are far less risky than experimental tokenized private credit pools.

Read the legal structure. The most important question is: if the issuer disappears tomorrow, what is your legal claim on the underlying asset? A good RWA product can answer that clearly. A bad one cannot.

Verify the audits. Reserve attestations and smart contract audits should be public. If they are not, treat that as a red flag.

Diversify. The same logic that applies to traditional portfolios applies on-chain. Concentration in a single token, issuer, or blockchain is concentration risk.

Keep records. Tax authorities increasingly expect on-chain activity to be reported. Use a portfolio tracker and keep transaction histories.

The Bigger Picture

Forecasts for the size of the tokenization market vary wildly. Some industry projections suggest tokenized assets could reach two trillion dollars by 2030. More aggressive estimates from major consulting firms run into the tens of trillions. Whether the final number is on the lower or higher end, the direction is clear: a meaningful share of the world’s financial assets is moving toward representation on public, programmable ledgers.

That shift will not happen all at once, and not every project will succeed. Many tokenized assets launched in 2026 will be forgotten by 2030. But the underlying idea — that ownership records, settlement, and compliance can live on shared infrastructure rather than in siloed databases — has crossed the threshold from theory to practice.

For investors, builders, and curious readers, this is no longer something happening “in crypto.” It is happening in finance, and crypto is simply the rail it runs on.

Frequently Asked Questions

Is RWA tokenization the same as buying cryptocurrency like Bitcoin? No. Bitcoin is a native digital asset with no claim on anything off-chain. An RWA token is a digital representation of a real-world thing — a bond, a building, a fund share — with a corresponding legal claim.

Are tokenized assets safe? “Safe” depends on the specific product, the issuer, the jurisdiction, and the risks discussed above. A tokenized U.S. Treasury fund from a regulated issuer carries very different risks from a tokenized private real estate deal in an emerging market.

Do I need a crypto wallet to access RWAs? Often yes, but increasingly, mainstream apps abstract the wallet away from the user. You may be holding tokenized assets without ever seeing a seed phrase.

Can I lose money on RWA tokens? Yes. Underlying asset prices can fall, smart contracts can fail, issuers can default, and liquidity can dry up. Tokenization changes the wrapper, not the fundamental risk of the asset inside.

What is the difference between a stablecoin and a tokenized money market fund? A stablecoin typically aims to hold a stable value (like one dollar) and may or may not pass yield to holders. A tokenized money market fund explicitly distributes the yield from its underlying portfolio to token holders.

Final Thoughts

The story of crypto in 2026 is no longer mainly about price predictions or memecoins. The deeper, slower, and more important story is that the financial system is being rebuilt on new infrastructure — and real-world assets are leading the way. Whether you are a long-term investor, a builder, or someone simply trying to understand where finance is headed, paying attention to RWA tokenization is no longer optional.

The next decade of finance will not be crypto versus traditional. It will be both, running on the same rails.

Disclaimer: This article is for educational and informational purposes only. It is not financial, investment, legal, or tax advice. Cryptocurrency and tokenized assets are volatile and risky. Always do your own research and consult a qualified financial advisor before making investment decisions. The author has no position in any specific token mentioned indirectly in this article.

Did you find this guide useful? Share it with someone exploring the future of finance, and bookmark this site for more original explainers on crypto, blockchain, and the digital economy.